Free ComGI Mock Exam Questions 2026: 4 Sample Questions with Answers (Commercial General Insurance)

Free ComGI (Commercial General Insurance) mock exam questions 2026. Test yourself with 4 sample questions covering Property, Business Interruption, Bonds, and Pecuniary Insurance with detailed explanations.

If you've passed BCP, you understand insurance principles. But ComGI is where you learn how those principles play out in the real world of business—where a single fire can cause millions in property damage, where a contractor's mistake can trigger a cascade of liability claims, and where an employee's dishonesty can threaten a company's survival.

Commercial insurance isn't just "bigger" personal insurance. It's a different game entirely:

- Sums insured often exceed $10 million (vs. $500K for a typical home)

- Policy structures involve complex clauses like "dual basis" payroll and "counter-indemnities"

- Stakeholders include contractors, principals, beneficiaries, and counter guarantors—not just the policyholder

The Business Mindset Shift

ComGI questions often test whether you can think like an underwriter advising a business client. Before attempting these questions, put yourself in this scenario:

"A manufacturing company approaches you for coverage. Their factory has $5M in machinery, employs 200 staff, and has ongoing construction contracts requiring performance bonds. What do they need to know?"

The questions below test concepts that would come up in exactly this type of client conversation.

These 4 ComGI practice questions cover Property Insurance, Business Interruption, Bonds, and Pecuniary Insurance—four areas where the commercial context changes everything you learned in BCP.

---

Question 1: Property Insurance (Chapter 1)

What is the usual period of insurance in a Fire Insurance policy?

A) 24 months

B) 18 months

C) 6 months

D) 12 months

Answer: D) 12 months

Explanation: Fire insurance policies are typically written on an annual basis, with the standard period of insurance being one year (12 months). Renewal is then considered at the end of this yearly term.

This is important to remember because:

- - Premium calculations are based on annual rates

- - Policy conditions and sums insured are reviewed annually

- - Inflation adjustments are typically applied at renewal

---

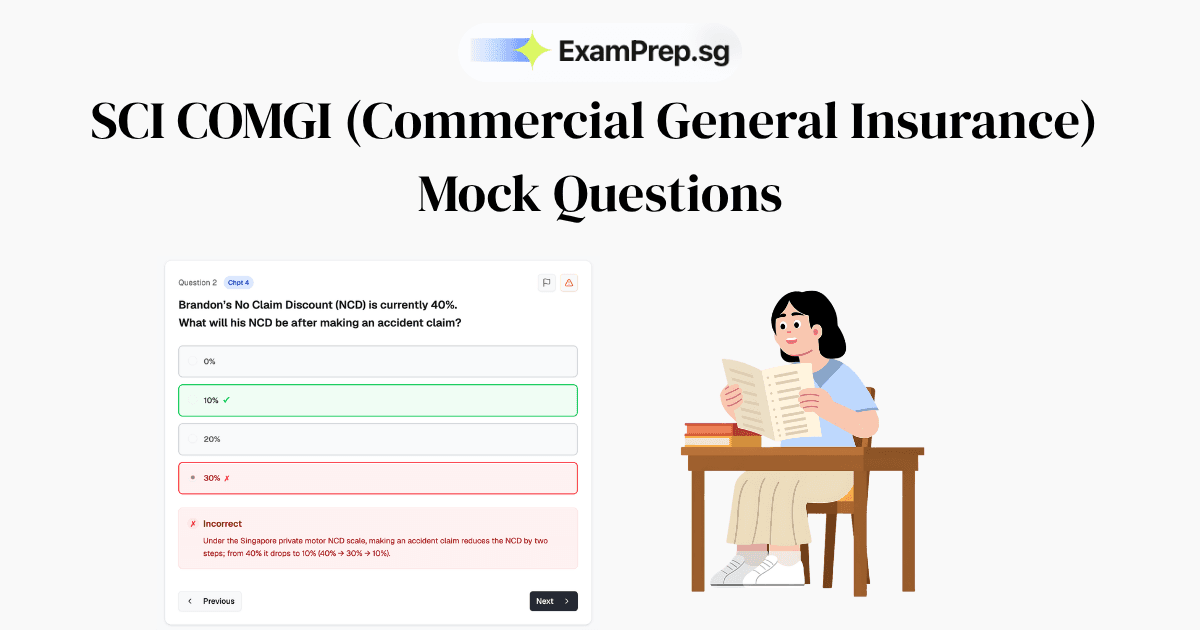

Question 2: Business Interruption Insurance (Chapter 2)

What is the usual percentage of payroll as per current practice in insuring payroll under a Business Interruption Insurance policy?

A) 75%

B) 50%

C) 25%

D) 100%

Answer: D) 100%

Explanation: Under Business Interruption insurance, payroll is usually insured at 100% because it represents the full wage bill that may continue to be payable during the interruption period.

Why 100%?

- - Staff salaries typically continue during business interruption

- - Retaining skilled employees is crucial for business recovery

- - Current practice is to cover the entire payroll unless the policy is specifically arranged on a limited payroll basis

Some policies may offer "dual basis" payroll coverage where a portion is insured for a longer period and the remainder for a shorter period, but the default practice is 100% coverage.

Practice with CMFAS Prep's Practice by Chapter mode to help you focus on your weak spots and drill down on specific chapters.

CMFAS Prep's Practice by Chapter mode helps you focus on specific chapters and master the concepts.

Question 3: Construction and Bond Insurance (Chapter 6)

During an internal training session on Bonds, Jett (a junior bond underwriter) learns that certain parties guarantee the insurer that they will pay for any losses incurred in the event that a claim is made.

These parties are known as:

A) Counter guarantors

B) Brokers

C) Reinsurers

D) Recovery agents

Answer: A) Counter guarantors

Explanation: In bond underwriting, counter guarantors provide a counter-indemnity to the insurer, guaranteeing to reimburse the insurer for any losses it pays under the bond if a claim occurs.

How it works:

- - An insurer issues a bond (e.g., performance bond, bid bond)

- - Counter guarantors sign an indemnity agreement

- - If a claim is made and the insurer pays out, counter guarantors must reimburse the insurer

- - Counter guarantors are typically the principal (contractor) and sometimes directors or parent companies

Why the other options are wrong:

- - Brokers facilitate insurance placement but don't guarantee losses

- - Reinsurers provide insurance to insurers but aren't counter guarantors

- - Recovery agents help recover losses after they occur

---

Question 4: Pecuniary Insurance (Chapter 7)

In a Fidelity Guarantee Insurance policy, whose monies is the employer obliged to retain and such amounts shall be deducted from any amounts payable by the insurer under the policy in the event of a loss?

A) Broker

B) Defaulting employee

C) Loss adjuster

D) Insurer

Answer: B) Defaulting employee

Explanation: Under a Fidelity Guarantee policy, any money of the defaulting employee that the employer is obliged to retain must be set off against the loss.

What this means:

- - If an employee commits fraud or theft, the employer must first deduct any amounts owed to that employee

- - This includes: unpaid salary, commissions, bonuses, leave pay, or other benefits due

- - These amounts are deducted from the insurer's claim payment

- - It's part of the employer's recovery from the employee

Example:

- - Employee embezzles $50,000

- - Employee has $5,000 in unpaid salary and benefits

- - Employer must retain the $5,000 and offset it against the loss

- - Insurer pays $45,000 (minus any excess/deductible) This principle ensures the employer doesn't receive double recovery.

CMFAS Prep provides instant feedback and explanations to help you understand the concepts better

Making Sense of Your Results

Got Question 2 (Business Interruption) right? Good—this is one of the trickiest ComGI concepts. Many candidates assume payroll would be partially insured (like 50% or 75%), but current market practice is 100%. This kind of "market practice" knowledge separates those who memorize from those who understand.

Struggled with Question 3 (Counter Guarantors)? Bonds are a unique product class that doesn't exist in personal insurance. Unlike a typical policy where the insurer pays the insured, bonds involve three parties: the principal (contractor), the beneficiary (project owner), and the insurer. Understanding who guarantees whom is crucial.

Question 4 (Fidelity Guarantee) caught you off guard? This tests the principle of avoiding double recovery—a theme that runs through all indemnity insurance but becomes especially important in pecuniary covers where cash flows between multiple parties.

ComGI vs. PGI: The Coverage Comparison

Still thinking in personal insurance terms? Here's how commercial insurance differs:

| Concept | PGI (Personal) | ComGI (Commercial) |

|---|---|---|

| Fire policy period | 12 months | 12 months (same, but sums are 10-100x larger) |

| Interruption cover | N/A for homes | Business Interruption—covers ongoing costs during shutdown |

| Third-party roles | Simple (insured + insurer) | Complex (counter guarantors, principals, beneficiaries) |

| Employee dishonesty | N/A | Fidelity Guarantee (with recovery offsets) |

CMFAS Prep's performance by chapter feature shows you your weakest chapters after every practice.

The ComGI Chapter Landscape

Unlike PGI where Motor Insurance dominates, ComGI distributes questions more evenly across its 9 chapters. Here's where to focus based on these sample questions:

| Chapter | Topic | What These Questions Reveal |

|---|---|---|

| 1 | Property Insurance | Standard terms like policy periods are tested (Q1) |

| 2 | Business Interruption | Market practices and coverage percentages matter (Q2) |

| 6 | Construction & Bonds | Understanding multi-party relationships is key (Q3) |

| 7 | Pecuniary Insurance | Recovery principles and offset rules are tested (Q4) |

The other chapters (Liability, Marine, Engineering, etc.) weren't covered in these 4 questions—but they're equally important on exam day.

The AI Recommendation Engine in CMFAS Prep creates personalized quizzes based on your weakest areas after every mock exam.

Your ComGI Preparation Path

If you found these questions straightforward: You're likely ready for full mock exams. The CMFAS Prep ComGI question bank has hundreds of questions across all 9 chapters.

If you need to strengthen fundamentals: Review our complete ComGI study guide for a chapter-by-chapter breakdown.

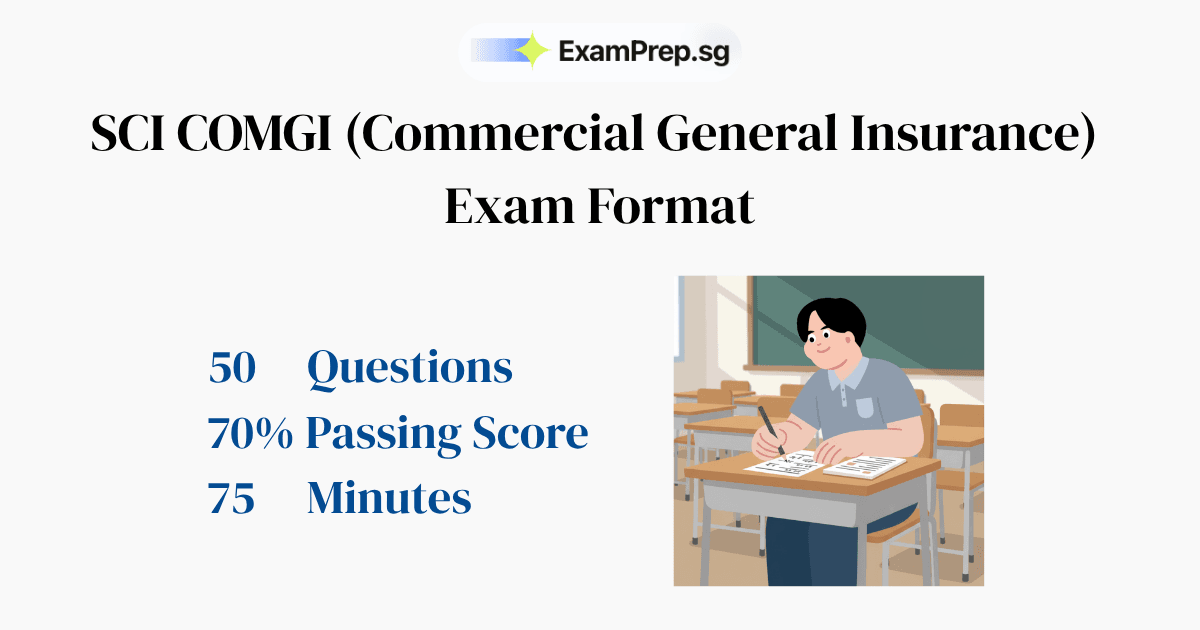

Not sure about the exam format? Read the ComGI passing score and format guide —50 questions in 75 minutes with a 70% pass mark.

Remember: ComGI isn't just about knowing the answers. It's about understanding how commercial insurance protects businesses in the real world.

Frequently Asked Questions About ComGI Mock Questions

Ready to Put This Strategy Into Action?

Ready for more practice? Access hundreds of ComGI questions with detailed explanations.

By The CMFAS Prep Team

Singapore's leading insurance exam preparation platform, helping thousands of candidates pass their certification exams on the first try.

Practise ComGI now

800+ exam-style ComGI questions with instant explanations.