Free PGI Mock Exam Questions 2026: 4 Realistic Exam Questions with Answers (Personal General Insurance)

Free PGI (Personal General Insurance) mock exam questions 2026. Test yourself with 4 sample questions covering Motor, Property, Travel, and Liability Insurance with detailed explanations.

You probably already own several PGI products without realizing it. That car insurance you renew every year? Motor insurance (Chapter 1). The travel insurance you bought for your Japan trip? Chapter 4. The coverage that came with your HDB flat? Personal property insurance (Chapter 2).

PGI tests your knowledge of insurance products that millions of Singaporeans use daily. Unlike BCP's abstract principles or ComGI's complex commercial scenarios, PGI is grounded in practical, everyday situations. The exam expects you to advise a customer on what their motor policy actually covers—and more importantly, what it doesn't.

Think Like a Customer's Insurance Adviser

PGI exam questions often present scenarios you'll face as an insurance representative:

- " My car was damaged in an accident. Why am I paying the first $500?" Excess (Q2)

- " The other driver was at fault. Can my insurer sue them?" Subrogation (Q3)

- " My luggage was stolen at the airport. Why won't you pay?" Baggage exclusions (Q4)

If you can explain these concepts to a frustrated customer, you can answer the exam questions.

These 4 PGI practice questions cover the products and principles you'll encounter most often—both in the exam and in real client conversations.

---

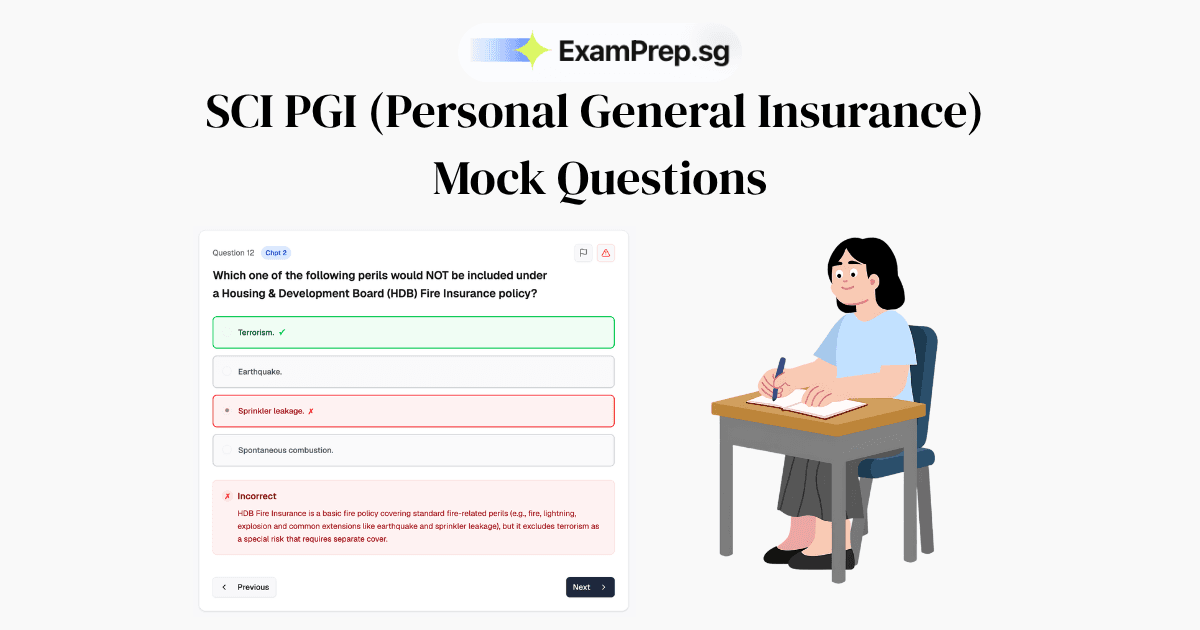

Question 1: Personal Property Insurance (Chapter 2)

Insurers are free to decide what perils to cover in Property Insurance.

A) TRUE

B) FALSE

Answer: A) TRUE

Explanation: Property insurance is a contract of indemnity and, subject to applicable laws/regulations and policy wording requirements, insurers can design their products by choosing which perils to insure and which exclusions/conditions to apply.

Key concepts:

- - Named perils — Policy only covers specifically listed perils (e.g., fire, lightning, explosion)

- - All-risks — Policy covers all perils except those specifically excluded

- - Insurers have flexibility in product design within regulatory boundaries

---

Question 2: Private Motor Car Insurance (Chapter 1)

What is an Excess?

A) The amount of loss that is claimable

B) The amount of loss that is unclaimable

C) Overpaid premiums

D) Additional claims not paid during the first claim

Answer: B) The amount of loss that is unclaimable

Explanation: An excess is the portion of each loss that the insured must bear themselves before the insurer pays. This means that part of the loss is not recoverable under the policy.

Example:

- - If you have a $500 excess and make a claim for $2,000 damage

- - You pay the first $500 (the excess)

- - Insurer pays the remaining $1,500

Why excess exists:

- - Eliminates small claims (administrative efficiency)

- - Encourages careful behavior by the insured

- - Keeps premiums lower

Note: Don't confuse excess with franchise. Excess is deducted from every claim; franchise is a threshold that triggers full payment.

CMFAS Prep has a feature that allows you to practice with realistic mock exams and get instant feedback and explanations to help you understand the concepts better.

CMFAS Prep provides instant feedback and explanations to help you understand the concepts better

Question 3: Personal Liability Insurance (Chapter 5)

Which of the following correctly describes subrogation?

A) The insurer need not pay any claims if the claims are fraudulent

B) The insurer has the right to pursue the wrong-doer in the insured's name

C) The insured must inform the insurer in writing of any change of circumstances which can increase the possibility of loss, injury or damage

D) The insurer and the insured have the right to cancel the policy if mutually agreed upon

Answer: B) The insurer has the right to pursue the wrong-doer in the insured's name

Explanation: Subrogation is the insurer's legal right, after indemnifying the insured for a loss caused by a third party, to step into the insured's shoes and recover the amount paid from the wrongdoer.

How subrogation works:

- - Third party causes damage to the insured

- - Insurer pays the insured's claim

- - Insurer then has the right to sue the third party (in the insured's name) to recover the payment

- - This prevents the insured from recovering twice (once from insurer, once from wrongdoer)

Why the other options are wrong:

- - A describes fraud (a separate principle)

- - C describes duty of disclosure

- - D describes policy cancellation terms

Drill into specific chapters with CMFAS Prep's Practice by Chapter mode.

CMFAS Prep's Practice by Chapter mode helps you focus on specific chapters and master the concepts.

Question 4: Travel Insurance (Chapter 4)

Which of the following is claimable under Personal Baggage benefit of a Travel insurance policy?

A) Loss of fragile or brittle articles

B) Loss to baggage left unattended

C) Value or repair of damaged baggage subject to policy limit

D) Loss to baggage sent in advance

Answer: C) Value or repair of damaged baggage subject to policy limit

Explanation: Personal Baggage covers the cost to repair or replace insured baggage that is lost or damaged during the trip, subject to the policy's limits and conditions.

Common exclusions (NOT covered):

- - Fragile or brittle items — Too prone to damage

- - Unattended baggage — Insured must take reasonable care

- - Baggage sent in advance — Not under the insured's control during the trip

- - Items left in unlocked vehicles

- - Valuables not in carry-on luggage

Key takeaway: Travel insurance baggage claims are subject to many exclusions. Always read the fine print and take reasonable precautions with your belongings.

Connecting Theory to Practice

PGI is unique among insurance exams because you can validate your answers against real-world experience. Let's see how:

Question 1 (Insurers' Freedom to Design Products): Think about how different insurers offer different home insurance products—some cover floods, some don't; some include accidental damage, others charge extra. This flexibility is why comparison shopping matters, and why you need to explain policy differences to customers.

Question 2 (Excess): Ever wondered why your motor insurance claim paid less than your repair bill? That's the excess at work. In Singapore, young drivers (under 27) often face additional excess because they're statistically higher risk. Understanding excess helps you explain premium structures to customers.

Question 3 (Subrogation): This is why your insurer asks "Was anyone else at fault?" when you make a claim. If another driver caused your accident, your insurer wants to recover their payout from that driver (or their insurer). It's not just a legal concept—it affects how claims are processed.

Question 4 (Travel Insurance Exclusions): This question reflects real claim rejections that happen every day. Customers are often surprised when their "comprehensive" travel insurance doesn't cover luggage they left unattended or items that were already in checked baggage. Knowing exclusions helps you set proper expectations.

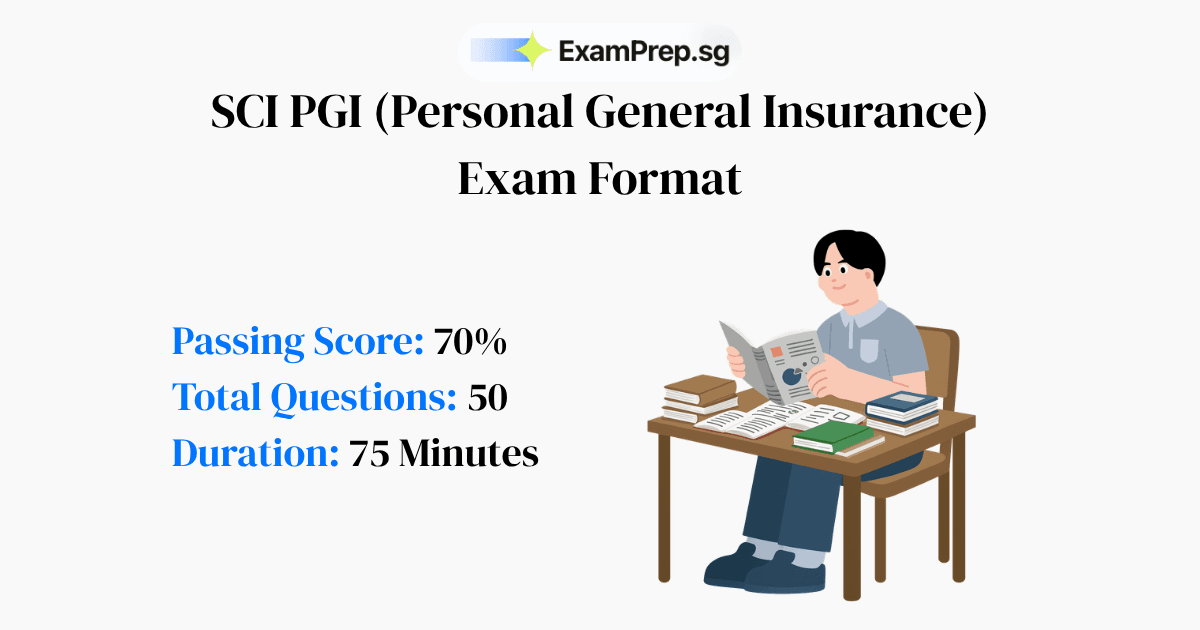

The PGI Exam Reality

50 questions in 75 minutes (1.5 min per question)—more relaxed than BCP but still requires steady pacing.

70% pass mark means you need 35 correct. You can afford 15 mistakes.

The key difference from BCP: PGI questions are more scenario-based. Instead of asking "What is subrogation?", they'll ask "In this situation, what can the insurer do?"

Practice Scenario-Based PGI Questions

CMFAS Prep's performance by chapter feature shows you your weakest chapters after every practice.

PGI's Product-Focused Chapters

Unlike BCP (concepts) or ComGI (business insurance), PGI is organized by product type. Each chapter is an insurance product you'll sell:

| Chapter | Product | Real-World Relevance | Question Volume |

|---|---|---|---|

| 1 | Private Motor Car Insurance | Singapore's most common insurance product | Slightly Higher |

| 2 | Personal Property Insurance | HDB/condo insurance | Medium |

| 3 | Personal Accident Insurance | PA riders on life policies | Medium |

| 4 | Travel Insurance | Pre-trip purchases | Medium |

| 5 | Personal Liability Insurance | Coverage for accidents you cause | Medium |

| 6 | Health Insurance (CI & Hospital Cash) | Increasingly popular products | Medium |

| 7 | FDW & Golfer's Insurance | Niche but tested | Lower |

Focus strategy: Chapter 1 (Motor) is the most heavily tested because it's the most commonly sold. Don't neglect Chapters 2-6, but if you're short on time, prioritize Motor.

The AI Recommendation Engine in CMFAS Prep creates personalized quizzes based on your weakest areas after every mock exam.

Building Your PGI Competence

Already passed BCP? Great—you have the foundation. PGI applies those principles (indemnity, subrogation, excess) to specific products. Our PGI study guide shows you how to build on that foundation.

Want to understand the exam structure? The PGI exam format guide breaks down the 50-question, 75-minute format.

Ready to practice seriously? The CMFAS Prep PGI question bank has hundreds of scenario-based questions with detailed explanations.

PGI certification, combined with BCP, gives you the credentials to sell personal insurance products in Singapore. These are products your friends and family already use—understanding them deeply is both professionally valuable and personally useful.

Frequently Asked Questions About PGI Mock Questions

Ready to Put This Strategy Into Action?

Ready for more practice? Access hundreds of PGI questions with detailed explanations.

By The CMFAS Prep Team

Singapore's leading insurance exam preparation platform, helping thousands of candidates pass their certification exams on the first try.

Practise PGI now

800+ exam-style PGI questions with instant explanations.