Free CMFAS M9 (CM-LIP) Mock Exam: Life Insurance Premium & Law Questions (2026)

Free CMFAS M9 (CM-LIP) mock questions with worked solutions. M9 is a separate exam from M9A — it tests life insurance principles, premium calculations & insurance law. 2026 syllabus.

M9 is NOT the same exam as M9A

The CMFAS M9 (also known as CM-LIP Part 1) is a completely separate certification from M9A. While M9A covers derivatives and structured products within ILPs, M9 focuses on life insurance fundamentals — including premium calculations (Gross/Net Premium), insurance law (Agency, Nominations), and policy provisions (APL, Non-Forfeiture). The question formats and required knowledge are fundamentally different. If you're looking for M9A practice questions on derivatives, visit our M9A mock exam page instead.

If you are preparing for the M9 exam, you likely fear two things: The Math and The Law.

Unlike RES 5 which tests ethics, the CMFAS M9 syllabus is technical. You cannot "common sense" your way through a Premium Calculation or a Trust Nomination question.

Most candidates look for free M9 mock exam papers to practice, but finding updated 2026 versions with step-by-step workings is difficult. We have compiled a list of the top 3 M9 mock exam providers here.

Below, we have created a free mini-mock covering the 5 concepts that cause the most failures: Premium Math, ILP Pricing, and Insurance Law.

TL;DR: The M9 (CM-LIP) "Technical" Trap

- The Math: You must know how to add/subtract "Loading" and "Expenses" correctly.

- The Law: Content heavy and difficult to memorize.

- The Fix: Use a simulator that shows step-by-step workings, not just the final answer.

- The Score: You need 70% (70/100 questions) to pass.

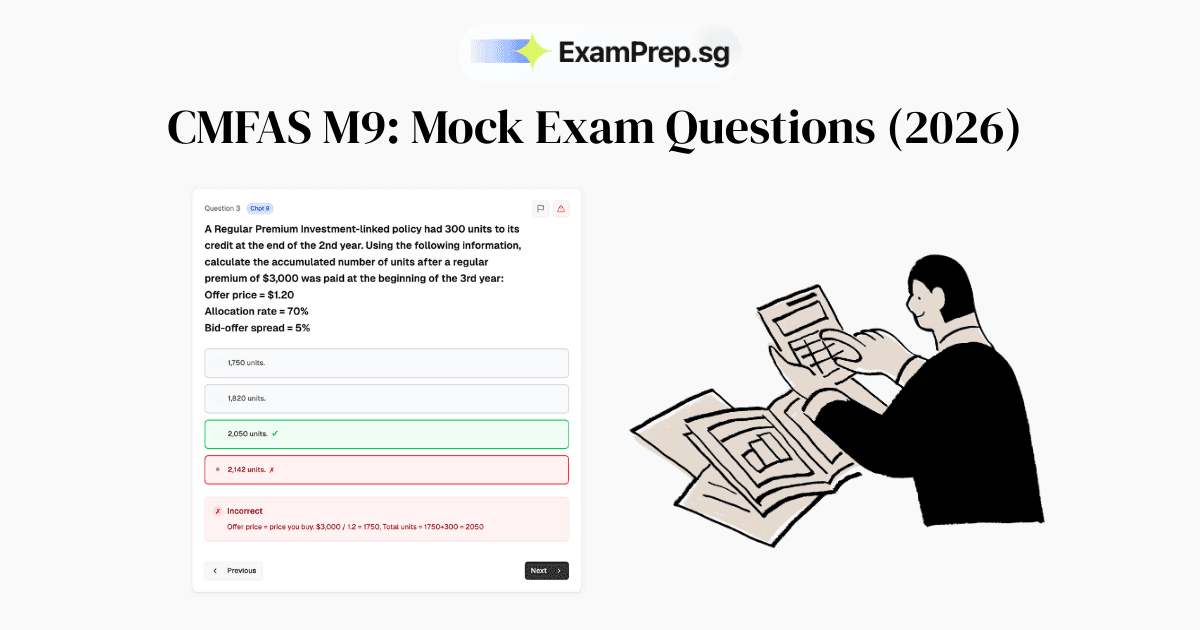

Question 1: Premium Calculation (Chapter 2)

Question: An insurance company uses the following data to calculate the premium for a policy: - Mortality Cost: $500 - Interest Earnings: $50 - Expenses: $100 - Buffer for Contingencies: $20

What is the **Gross Premium**?

- A) $550

- B) $570

- C) $450

- D) $670

The Trap: Candidates often forget whether "Interest" should be added or subtracted.

The Correct Answer: B ($570)

The Logic:

- Net Premium = Mortality Cost - Interest Earnings ($500 - $50 = $450).

- Gross Premium = Net Premium + Expenses + Buffer ($450 + $100 + $20 = $570).

Our simulator shows the exact formula and substitution for every calculation question, so you never have to guess.

---

Question 2: Insurance Nomination (Chapter 17)

Question: AWhich one of the following statements regarding the new Nomination of Beneficiaries (NOB) framework is TRUE?

- A) Making a nomination under the new regime is compulsory.

- B) Revocable nominations are allowed under the new framework.

- C) The new NOB is governed under Section 73 of the Conveyancing and Law of Property Act 1886.

- D) One of the aims of the NOB is to accord greater financial protection to policy owners from life insurance companies.

The Correct Answer: B

The Logic: Revocable nominations are permitted under the new NOB framework, allowing policy owners to modify or revoke their nominations, which provides flexibility and control over the policy benefits.

Having trouble reading the entire textbook?

This specific topic accounts for ~5-8 questions in the exam. Our platform has a dedicated "Practice by Chapter" mode to help you drill on your weakest chapters.

Try the M9 Exam Simulator (Free Demo)

Question 3: ILP Pricing (Chapter 9)

Question: An Investment-Linked Policy (ILP) operates on a **Forward Pricing** basis. A client submits a redemption request at 2:00 PM on Tuesday. The cut-off time is 3:00 PM. Which price will apply?

- A) Tuesday's closing price (calculated on Wednesday).

- B) Tuesday's opening price (calculated on Monday).

- C) Wednesday's closing price.

- D) The price at the exact moment of transaction (2:00 PM).

The Trap: Candidates assume "Forward" means "Next Day."

The Correct Answer: A

The Logic: "Forward Pricing" means the price is not yet known at the time of transaction. Since the request was before the cut-off (3 PM), it will use Tuesday's Valuation Price, which is typically calculated/published the next working day (Wednesday), but it represents Tuesday's value.

---

Question 4: Law of Agency (Chapter 15)

Scenario: An agent, whose license has expired, collects a premium from a client. The insurance company accepts the premium, unaware of the expiry. Later, the company discovers the error but decides to honor the policy anyway.

Question: This is an example of agency by...?

- A) Estoppel

- B) Ratification

- C) Necessity

- D) Agreement

The Trap: All options are legal terms that look similar.

The Correct Answer: B

The Logic: Ratification occurs when a principal (Insurer) retrospectively confirms an unauthorized act done by the agent. By accepting the premium and honoring the policy after the fact, they have "ratified" the agent's action.

---

Question 5: Non-Forfeiture (Chapter 4)

Question: A Whole Life policy has acquired a Cash Value. The policyholder stops paying premiums but does not terminate the policy. The insurer automatically advances the premium from the Cash Value to keep the policy in force.

Question: What is this provision called?

- A) Paid-Up Policy

- B) Extended Term Assurance

- C) Automatic Premium Loan (APL)

- D) Surrender

The Trap: Confusing APL with Paid-Up.

The Correct Answer: C

The Logic: APL acts as a loan. The insurer lends you the premium money from your own cash value (with interest). The policy coverage remains identical. (In contrast, a "Paid-Up" policy reduces the Sum Assured).

---

Why M9 Calculations are Dangerous

Did you get Question 1 (Premiums) correct?

The exam has roughly 15-20 calculation questions. If you memorized the definitions but don't know the formulas for Net Premium or Bid-Offer Spread, you are walking into the exam with a handicap.

How to Fix It:

You need to practice the math until it becomes muscle memory. We have written a full deep-dive on the difficulty of the M9 exam, as well as it's killer chapters here.

At CMFAS Prep, our M9 Simulator includes:

-

Step-by-Step Workings: We don't just give the answer; we show the formula.

-

Law Drills: Dedicated "Practice by Chapter" mode to help you drill on your weakest chapters.

-

2026 Updates: All questions match the latest SCI syllabus.

Don't leave your pass/fail result to chance.

Frequently Asked Questions About M9 (CM-LIP) Life Insurance Exam

Ready to Put This Strategy Into Action?

Master M9 (CM-LIP) life insurance calculations and law with step-by-step explanations. Practice until the formulas become muscle memory.

By The CMFAS Prep Team

Singapore's leading CMFAS and SCI exam preparation platform, helping thousands of candidates pass their financial adviser exams on the first try.

Practise M9 now

800+ exam-style M9 questions with instant explanations.